AI and analytics in finance: how CFOs and FP&A teams improve forecasting, budgeting, and reporting

June 2, 2026/9 min read/Team Dataiku

Finance teams have more data than they can act on. Transactions stream in from enterprise resource planning (ERP), general ledger (GL), accounts payable and receivable (AP/AR), market feeds, and treasury systems around the clock. But by the time that data reaches a decision, the moment has often passed.

The bottleneck is the gap between what analytics can surface and what teams can do with it, fast enough to matter. Closing that gap is what AI-driven decision intelligence does. Dashboards explain what happened last quarter. Predictive models tell you what is likely to happen next week. AI-assisted workflows route the right signal to the right person before the window closes.

This guide looks at AI and analytics in finance from the CFO's seat: what's changing in financial planning and analysis (FP&A) and financial reporting, and how finance teams are using AI to make faster, better-supported decisions. You will see what the shift from descriptive analytics to AI-driven decisions looks like operationally, and what your platform, data, and governance need to support it.

AI for FP&A teams has moved past static reporting. It now drives forecasting and budgeting decisions on live data, with governance built into the workflow.

FP&A use cases (cash flow forecasting, driver-based budgets, expense anomaly detection) deliver the fastest measurable wins.

Real-time reporting and NLG-driven commentary compress the monthly close and cut manual variance work.

Dataiku connects finance data sources, ML models, agents, and governance controls into one orchestrated workflow, from first experiment to production.

Analytics and AI in finance refers to the use of machine learning, statistical modeling, and data orchestration to support financial operations across both backward-looking reporting and forward-looking decisions. Rather than describing what happened, these systems score what is likely to happen, flag what requires attention, and surface the context a decision-maker needs to act.

Analytics in finance has always meant turning transactions into reports. AI extends that work in two directions. ML finds patterns across transaction histories, payment behaviors, and cost drivers that no rule-based model would catch. Advanced analytics combines those patterns with business logic and external signals so the finance function can decide, not just describe. The data sources are familiar:

ERP and general ledger systems for transaction records

Subledgers for AP/AR

Market feeds for foreign exchange (FX) rates

Customer relationship management (CRM) systems for revenue intent

Operational systems for cost drivers

What has changed is the volume and velocity. A monthly close that depended on spreadsheets five years ago now depends on millions of rows pulled from a dozen platforms each day, and manual reconciliation cannot scale to that surface area.

That gap is where decision intelligence operates: connecting data, models, and human judgment in one place so the forecast or the anomaly flag reaches the person who can act on it before the moment passes.

A working AI platform for finance has four layers:

1. The data lakehouse holds transactional history and operational context.

2. Above it, a shared analytics layer keeps engineered signals drawn from ERP and GL systems, including rolling balances, payment patterns, and variance drivers, reusable across teams.

3. ML and natural language processing (NLP) engines train and serve the models.

4. Business intelligence (BI) and visualization push the results back to the people running the close, the budget, or the board.

Finance decision cycles touch every one of those layers. A 13-week cash forecast, for example, needs daily transaction feeds, engineered seasonality features, a trained forecasting model, and a dashboard the treasurer trusts. Drop any single layer, and the workflow stalls before it reaches a decision.

For finance teams specifically, security, governance, and infrastructure flexibility are not optional add-ons. Finance data lives across cloud, on-prem, and air-gapped environments simultaneously, which means models must be auditable, roles must be enforced, and logs must be tamper-evident at every layer.

Dataiku, the Platform for AI Success, is the orchestration layer that connects all of this. Finance data sources, ML models, AI agents, and governance controls run in one workflow, eliminating handoffs. Dataiku's model capabilities give finance teams a governed path from experimentation to production for FP&A forecasting and budgeting models, with controls embedded at every step rather than assembled at the end.

The pain points in FP&A are consistent across organizations: Forecasts arrive too late to influence decisions, carry analyst bias baked in during manual assembly, and require weeks of variance work before they are ready to present. AI addresses each of those problems at the source.

Time-series ML models ingest AR and AP patterns, customer payment behavior, and seasonal effects to produce daily or monthly cash positions. Daily granularity matters for treasury operations; monthly is enough for quarterly planning. The model learns from history but updates the moment a large invoice clears or a major customer slips.

What makes the forecast operationally useful is driver mapping: Each prediction connects back to the specific signal that moved it, whether a delayed shipment, a discount taken, or a renewal not yet booked. Treasury sees not just the number but the reason behind it, which turns a forecast from a static deliverable into a decision input the cash team can act on within hours.

Regression and gradient-boosted models replace the annual budget cycle with continuous driver updates. Sales volume, FX rates, commodity prices, and headcount feed in as live inputs, and the model rebuilds the budget bottom-up as those inputs shift. When a line drifts past a defined variance threshold, an alert fires automatically.

The output lands in the dashboard the FP&A team already uses, so there is no separate model interface to learn. Analysts see live drivers, the impact on the bottom line, and the alerts that need a human judgment call, all in one view.

Travel, entertainment, and procurement claims vary enough that rule-based filters miss most exceptions. Unsupervised learning addresses this by flagging claims that fall outside normal patterns for the employee, the cost center, or the vendor, catching duplicate submissions and miscategorized expenses that manual review would not surface. Review hours fall sharply because the system escalates only a small share of claims that look genuinely unusual, rather than every submission.

Every flag carries a record of who reviewed it, what was approved, and why a claim was paid or returned, giving the finance team a defensible record without chasing emails.

The measurable benefits show up in two places: Forecast accuracy lifts by enough percentage points to change quarterly guidance, and close cycles compress from weeks to days.

Well-documented, explainable models are what make automated reporting defensible. That's what allows the monthly close to compress once finance teams stop assembling reports by hand. Large language model (LLM)-assisted tools read the variance tables, draft the commentary, and return the analyst's time to judgment work rather than formatting work.

Embedded BI gives the CFO a board-ready view and the analyst a transactional drill-down from the same underlying dataset, with role-based access controlling what each role can see. In-memory calculation engines slice and re-aggregate large datasets in well under a second, so a sensitivity question raised in a planning meeting gets answered before the conversation moves on.

The practical result is fewer one-off requests in the analyst's inbox: The CFO checks the metric directly, and the analyst redirects those recovered hours to the next forecast cycle.

Natural language generation (NLG) converts variance tables into readable commentary, explaining what moved, by how much, and against which driver in language a non-financial reader can follow. Because templates are governed, the output stays consistent across business units and quarters, and audit trails record which model generated which paragraph.

The same NLG layer extends directly to quarterly board packs, producing executive summaries, segment narratives, and variance callouts without a separate authoring pass.

The KPIs to watch: report preparation hours per close, CFO query turnaround time, and the share of commentary requiring analyst rewrite.

AI in finance is rarely a single project with a defined end date. It's a sequence of capabilities, each built on shared data, shared models, and shared governance, and the order in which you build them shapes the speed and size of the payback.

Start with a structured inventory of which systems hold which financial records, who owns them, and what quality each delivers. Scoring against completeness, timeliness, and accuracy produces a baseline scorecard. Lineage mapping shows how records flow from source to report, building the documentation trail regulators will eventually ask for.

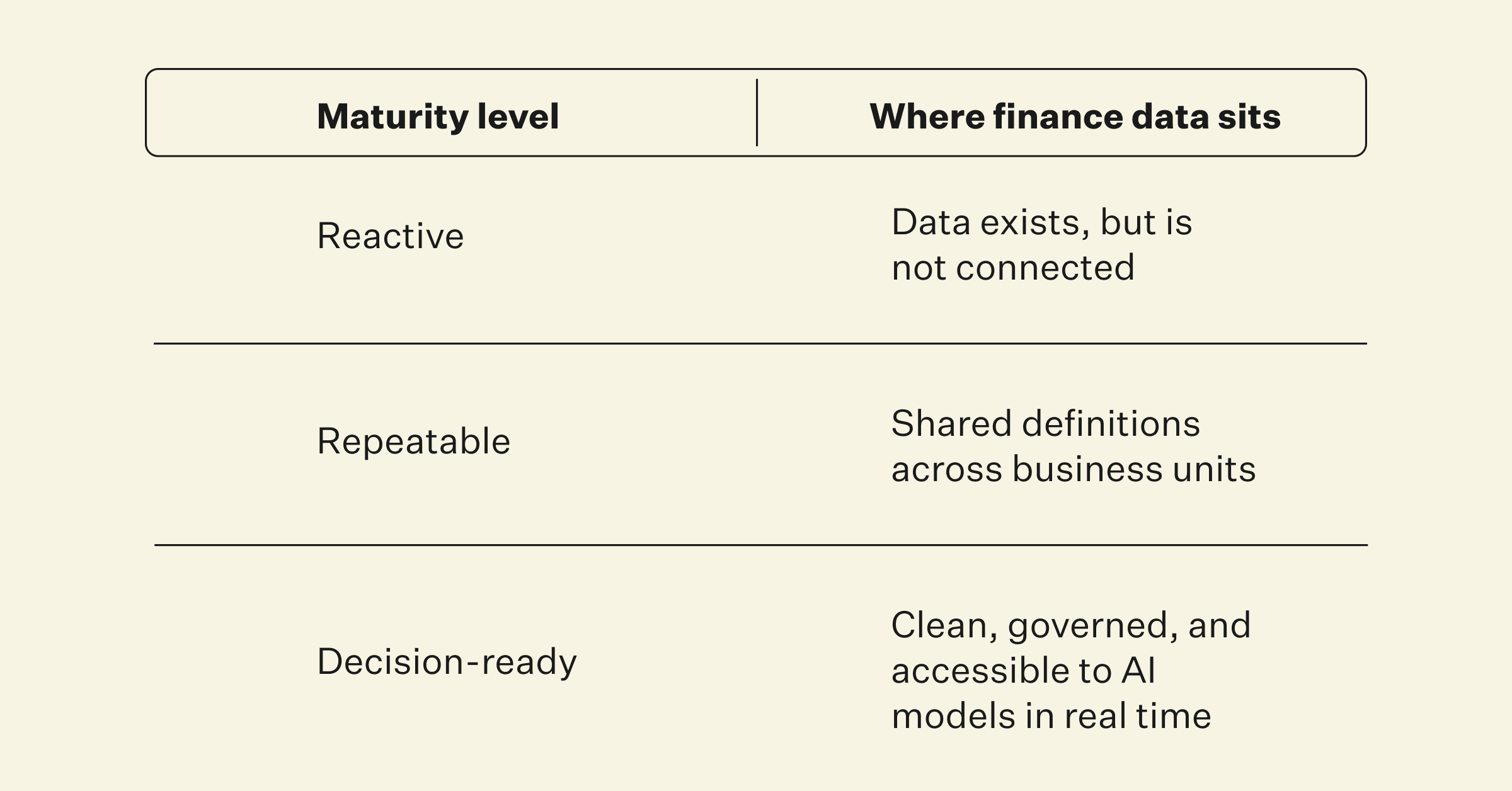

A simple three-level maturity scale helps frame the next move:

Click on the image above to zoom into full PDF

Most finance functions sit in "Repeatable." Decision-ready is the target.

Governance for finance AI rests on three pillars: policy documentation, version control, and explainable AI (XAI) dashboards. Sarbanes-Oxley requires management to assess and evidence the internal controls over financial reporting, which means any model feeding a reported number needs to sit inside a documented control environment, even though the statute itself doesn't speak to AI or model explainability directly.

In practice, auditors increasingly expect that standard to extend to the models themselves: documented, explainable behavior before a model reaches the close or the forecast, not after-the-fact justification.

Dataiku Govern provides the model registry, lineage, version control, and explainability dashboards built to support audit, internal controls, and financial reporting requirements. Dataiku Visual ML includes SHAP and partial dependence plots that satisfy auditor documentation expectations without additional tooling. For an overview of enterprise AI governance and regulatory requirements, check out this playbook from Dataiku.

The formula is straightforward: (Benefit − Cost) / Cost

The work is in defining each side.

Benefits fall into three buckets: Productivity covers hours returned to FP&A, treasury, and reporting teams. Loss avoidance covers reporting errors caught before publication and budget overruns avoided before they compound. Revenue uplift covers better forecasts that improve pricing decisions, working capital management, or capital allocation.

Cost has four lines you need to defend:

Platform licenses

Model build effort

Integration work

Ongoing governance overhead

ROI calculated this way gives the CFO a number grounded in the organization's own operations, not a vendor-supplied benchmark. When evaluating a finance AI partner, look for a practical checklist covering data integration depth, model governance tooling, explainability capabilities, deployment flexibility, and a verifiable path from pilot to production.

Most finance AI programs don't stall because the use cases are wrong. Rather, the infrastructure underneath the AI programs is fragmented. Models sit in one tool, governance in another, and agents somewhere else entirely.

Dataiku is the orchestration layer that connects all of it. DigiKey's accounts receivable team used Dataiku to automate payment reconciliation, a process that once required manual interpretation of cryptic bank notes across multiple currencies and file formats. Today, AI assists with 92% of incoming payment receipts, and 62% are auto-applied with no human review at all, freeing the team from mandatory overtime and backlog buildup to focus on higher-value work.

For finance organizations ready to move from individual use cases to a production AI program, Dataiku's Finance and Audit capabilities connect FP&A forecasting, budgeting, and reporting into one governed workflow rather than a scatter of disconnected tools.

The data, the ML models, the agents, and the business rules sit in one orchestrated platform, with governance applied as the work happens rather than bolted on at audit time. The intelligence your team builds becomes an asset you own, not a dependency you manage.

Together, analytics and AI move finance teams from reactive reporting to predictive decisioning. Forecasts get sharper, budgets update against live drivers instead of a static annual cycle, and reporting becomes a live conversation with the data rather than a once-a-month deliverable.

Decision-making applications use ML for forecasting, driver analysis, and anomaly detection. Reporting applications use NLG for commentary and self-service BI for live dashboards. Underneath both, governance controls track every model version, every decision, and every dataset, so finance leaders can defend the outcome.

Three challenges show up in almost every program: fragmented data across ERP, GL, and operational systems; uneven model governance that surfaces only at review time; and a skills gap between FP&A analysts and the small number of data scientists who understand both finance and ML. Implementation cost can run from the low six figures for a targeted use case to seven figures for a multi-use-case platform program.

A minimum useful footprint is a lakehouse or warehouse with clean transactional data, a feature store for reusable signals, ML training and serving infrastructure, and a governance layer covering lineage, versioning, and access. Cloud-native deployments are common; regulated firms often run hybrid or on-prem. Data volumes vary, but most production finance models need at least two to three years of clean history.

Targeted FP&A and anomaly-detection use cases typically pay back within two to four quarters because the productivity gains and loss-avoidance savings are easy to measure. Reporting and NLG-driven use cases follow a similar timeline, often six to nine months to move from pilot to full adoption, with ongoing gains as the model improves with feedback. The fastest path to ROI is starting with one well-scoped use case, proving the governance pattern, then scaling.